New Growth Drivers for Industrial Upgrading: Green Energy Transition and Digital Transformation

As Vietnam experiences rapid economic growth, its agricultural sector experiences a hollowing-out as urban centers absorb cheap human capital to increase industrial production.

Fig 1. Share of Agriculture in Vietnam’s economy has been decreasing since 2011. Source: Statista

However, this one-way absorption will eventually slow down as labor becomes increasingly scarce. Industrial sectors will therefore be compelled to raise wages to address the dwindling labor supply, resulting in productivity losses as the aggregate supply curve begins to curve up.

Fig 2. Graphical illustration of the Lewis Turning Point using the neo-classical model of Aggregate Demand and Supply. Source: Research Gate

This will induce the Lewis Turning Point, and Vietnam would need to address this structural challenge through technological transformation and a shift to capital-intensive, rather than labor-intensive, output.[1] In graphical terms, this means shifting the aggregate supply curve outwards such that productivity losses will be minimized as wages decrease once more. Such exigence was seen in the Vietnamese Prime Minister’s outlook for 2025, in which he emphasized the importance of “renewing traditional growth drivers.” [2] There are two broad directions where Vietnam has already poised itself for development: The Green Transition, and the Digital Transformation.

Green Transition

Vietnam’s dedication to the Green Transition can hardly be understated. There have been concerted government efforts to both attract foreign investors in the space and introduce domestic policies to encourage renewable-energy driven growth. For example, the government has been proactive in attracting FDI for renewable energy projects, especially in the industrial real-estate sector.[3] Japan's Shizuoka Gas has recently acquired a 25% stake in a solar power plant in Ninh Thuan province, and Germany’s PNE AG is waiting for the official green light for the construction of a $4.6 billion USD, 2000 MW off-shore wind project.[4] [5]Additionally, recently updated regulations to Green Credit have also spurred creation and demand for Green Bonds/Loans by introducing preferential loan terms 0.5-2% lower than market rates for green-energy projects.[6] [7]

These activities are undergirded by legislative changes. Vietnam’s PDP8 Implementation Plan, an ambitious master plan for the next decade that seeks to achieve Vietnam’s net-zero carbon emissions by 2050, has been introduced this April. Additionally, the recent implementation of the Electricity Law will also incentivize greater green-energy investment by according green-energy projects Direct Power Purchase Agreements (DPPAs). Such agreements exclude them from the competitive bidding process for energy tariffs as they can circumvent the utilities sector by directly providing energy to consumers.[8] This is also significant as it allows the energy sector to be less dependent on Vietnam’s underperforming utilities sector, which has been bogged down by under-capacity and occasional blackouts.[9] Recent regulations in December have also addressed existing legal loopholes in wind energy investment, providing timely remediation following high-profile investor exits that cited a lack of regulatory clarity as the main issue.[10] [11] These updates included minimum long-term purchase agreements, land/sea rental deductions, and the prioritization of green energy in the national grid.[12] Even though regulatory hurdles remain the main obstacle, an eager government goes a long way in reducing existing roadblocks for greater growth in the sector.

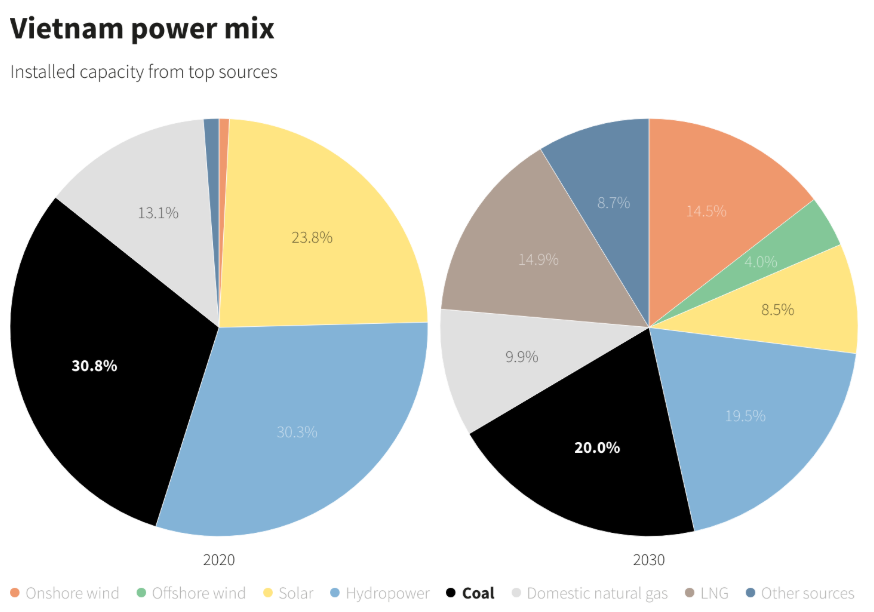

Fig 2. Vietnam’s power composition from 2020 to 2030; Wind Energy and LNG will experience the largest increase. Source: Vietnam Briefing

Looking at the next decade, there are clear incentives to increase wind and LNG projects, whose growth would be more-than-proportionate to the increase in total energy consumption. Of these 2, we see the most drastic increase in LNG percentage, which comes at a backdrop of anemic domestic supply due to aging infrastructure and depleting reserves in the Nam Com Son and Cuu Long Basins. Increasing urbanization and projected high manufacturing output means that power-hungry Vietnam needs to balance its long-term objectives of net-zero emissions with economic growth: LNG is more power efficient (roughly a 50-60% energy conversion rate for standard models) and has greater capacity usage than other renewable energy sources. [13] However, LNG power supply faces the greatest uncertainties. High fixed and marginal costs associated with LNG imports would also indicate higher electricity tariffs, which might not be economically viable for Vietnam’s consumer class. This has been exacerbated by price-cap controls by the government to preserve affordability. This has deterred foreign investors and has further weakened Vietnam’s bargaining power given high demand for the resource from regional peers in the near future.[14] [15] Government decrees in August set a $12.9792 per million British thermal units (mmBtu) price ceiling, which barely breaks even with existing Asian spot rates for LNG.[16]

Fig 3. Vietnam’s imposed price ceiling on imported LNG will not easily persuade foreign suppliers and investors. Source: International Monetary Fund, FRED, Reuters.

Depreciation pressures on the Dong in 2025 would also increase costs. Moreover, recent regulatory positions remain uncertain regarding the critical issue of Guaranteed Minimum Purchases by the national grid—an industry-standard practice for LNG suppliers to mitigate price fluctuations. [17]

Conversely, Wind Power seems to have the greatest potential. With its 3,000-km-long coastline and high wind speeds in coastal areas, Vietnam has an impressive wind power potential of 650 GW. This surpasses all its regional peers in renewable energy adoption prospects.[18] Additionally, recent revisions in December to the new Electricity Law have further assured international investors about the regulatory environment in Vietnam by clarifying conditions under which FDI can take part in infrastructure development. Some policies include exemption from sea/land area usage fees during construction, rental fee reductions post construction (Article 6, 22) and reduced corporate taxes (10% for first 15 years). More importantly, a limit of ownership ratio of foreign investors to 50-65% of renewable-energy projects is set to benefit local enterprises primarily through the form of increased revenue and technological spillover. [18] This indicates that domestic companies would now be more directly implicated in the green energy transition. Fundamentally, developing reliable, domestic energy sources help hedge external shocks for Vietnam’s highly interconnected economy. While LNG’s short-term efficiency seems to be an advantage, complicating factors and medium-term considerations would likely be overweight on renewable energy—particularly wind energy—development.

Digital Transformation

Vietnam’s digital transformation has been the second key driver for greater labor productivity, which has been lagging its regional competitors.[19] Such transformation is constituted of greater connectivity, better digital infrastructure, and eventually a more robust digital-physical infrastructure (IOT). The government plans to achieve comprehensive 5G network coverage by 2030, and government-owned Viettel Group has recently rolled out the nation’s first 5G network plan in October. [20] [21] However, telecommunications equities in Vietnam have been consistently underperforming. The telecommunications industry only has a CAGR forecast of approximately 1 percent from 2021-2027, since the digital infrastructure has already been highly developed: 4G coverage is at 99.8%, while the number of smartphone users hovers around 84% of the population.[22] This has significantly reduced the Total Addressable Market (TAM), a trend further accelerated by the widespread adoption of Over-The-Top (OTT) messaging and chat services like Zalo (used by 87% of the population in 2022), Messenger, and Telegram, which have largely replaced traditional Telecommunications revenue streams such as voice calls and SMS. Most importantly, the telecommunications industry in Vietnam is largely dominated by SOEs, leaving little possibility for potential entrants in an industry with high capital barriers. This limits portfolio diversification and increases the exposure and vulnerability of our investments.

However, opportunities do lie in the energy sector following concurrent developments in improving digital infrastructure. On November 30, the government passed amendments on the Data Law, a piece of comprehensive legislation concerning data protection, collection, and transfer. This development arrives in tandem with cutting-edge technology investments in Vietnam from both domestic (FPT, VinGroup) and international investors (Samsung, Nvidia) which seek to build data centers and capital-intensive R&D hubs.[23] Clearer regulations would indicate a better business environment for these R&D hubs, which collect consumer data to innovate and improve their products. These energy-intensive operations would require a stable source of electricity, and recent developments in DPPA regulations would allow these companies to bypass the underperforming Electricity of Vietnam (EVN) and source clean, renewable energy directly.[24] Samsung announced in July their plans to procure energy directly from the source to power their data centers, while Nvidia’s $200 million USD data center would also likely utilize DPPAs to support its energy consumption.[25] [26] Locally, FPT Software, the largest domestic data provider in Vietnam, has also collaborated with USAID to achieve net-zero emissions by 2040.[27]

In summary, Vietnam’s new developments are an economic necessity for a developing nation playing catch-up. Current analysis shows exciting opportunities in different sectors of innovation, and how they will translate to the equity market. As Vietnam’s stock exchange prepares to enter the “emerging market” status by 2026, the VN index is well-poised for massive growth following potential credit rating increases, inclusion in the MSCI Emerging Markets Index, and greater passive fund tracking. However, the VN-index is seemingly historically undervalued, with forward P/E ratios hovering at a 10-year low.

Fig 4. Forward P/E for VNI/Vietnam Ho Chi Minh Index indicate possible undervaluation of Vietnamese equities. Source: Bloomberg, VCG, Vina Capital.

The main catalyst for such depressed valuation is probably due to massive financial outflows following the weak performance of the Dong and recent political instability.[28] This is, however, not reflective of strong intrinsic performance. With a reviving real estate and financial sector, Vietnam bets on new economic accelerators to hedge against a slightly pessimistic export scenario in 2025.

References

[1] United Nations Development Programme. (2024, March 15). Core principles of growth still apply.

[2] VietnamPlus. (2024, March 20). Prime Minister urges promotion of new growth drivers.

[3] Vietnam Investment Review. (2024, July 15). Green capital flowing into industrial real estate in Vietnam.

[4] S&P Global Commodity Insights. (2024, November 15). Vietnam's 2025 energy demand spike fuels renewable investment boom.

[5] The Investor. (2024, October 10). Germany's PNE ready to deploy $4.6 bln offshore wind power project in central Vietnam: CEO.

[6] Green Central Banking. (2024, August 28). Vietnam central bank introduces green credit framework.

[7] Vietnam Investment Review. (2024, September 10). Legal framework critical to boosting green credit.

[8] Allen & Overy. (2024, June 5). Vietnam's new electricity law: A new beginning.

[9] McKinsey & Company. (2024, May 10). Putting renewable energy within reach: Vietnam's high-stakes pivot.

[10] Reuters. (2024, August 23). Equinor halts Vietnam offshore wind plans, to close Hanoi office.

[11] Watson Farley & Williams. (2024, September 15). Vietnam offshore wind: Status and recent developments.

[12] Baker McKenzie. (2024, December 18). Vietnam offshore wind draft: New regulations released for public comments.

[13] IPIECA. (2022, November). Combined cycle gas turbines.

[14] Shell. (2024). LNG outlook 2024.

[15] Reuters. (2024, August 1). Vietnam's LNG price cap puts gas-fired power target at risk.

[16] Vietnam Electricity. (2024, July 20). Ministry approves base price for LNG-fired power at 10.56 US cents/kWh.

[17] Allen & Overy. (2024, June 5). Vietnam's new electricity law: A new beginning.

[18] Ibid.

[19] McKinsey & Company. (2024, April 25). Capturing the wind: Renewable energy opportunities in Vietnam.

[20] GovMedia. (2024, May 10). Vietnam's new strategy to cover 99% of the population with 5G.

[21] Datacenter Dynamics. (2024, June 1). Viettel launches Vietnam's first 5G network.

[22] Statista. (n.d.). Telecommunications industry in Vietnam.

[23] OpenGov Asia. (2024, December 10). Vietnam driving AI innovation with new research and data centres.

[24] World Resources Institute. (2024, April 5). Vietnam's direct power purchase agreement: Path to renewable energy expansion.

[25] Samsung Newsroom. (2024, November 20). Samsung Electronics Vietnam accelerates its climate action by expanding renewable energy procurement.

[26] U.S. News & World Report. (2024, December 5). Nvidia signs AI cooperation agreement with Vietnamese government.

[27] FPT Software. (2024, July 30). FPT cooperates with USAID to promote clean energy deployment, reduce greenhouse gas emissions, and accelerate net zero transition.

[28] Reuters. (2024, May 17). Foreigners sell Vietnam securities amid political turbulence, data show.